ramble |ˈrambəl|verb [ no obj. ]1 walk for pleasure, typically without a definite route.• (of a plant) put out long shoots and grow over walls or other plants.2 talk or write at length in a confused or inconsequential way.

Boss Zuckerberg

I'm a lucky PhD supervisor: these days, my PhD students are all very productive, working on some really nice new papers. I am happy (and honored) to be a co-author on some of those papers. Others are written with other co-authors (and that too makes me happy).

One tricky thing with being a PhD supervisor, is getting the PhD student to own the paper: realizing that he/she is in the drivers seat. Apart from many other things, there is of course one consequence of being in charge of a paper ánd having me as a co-author: having me as a co-author. Things get worse, when I am not just your co-author, but also your PhD supervisor….

I will not bore you with the details. My point is simply: leadership is not just determined by who is in charge. No. Really not.

What reminded me of this was an article published about two weeks ago in the NY Times. The topic of the article: Mark Zuckerberg. I am not on Facebook, nor do I want to be (I know, the whole blog thing is pretty ironic). But I do know who Mark (can I say Mark) is. The article discussed the way in Mr. Zuckerberg has managed to be in control of Facebook, before and after the IPO. The article takes a pretty narrow, but very appropriate, definition of control, and focus on Mr. Zuckerbergs' shareholdings and voting rights.

In the words of Charles Elson, professor of corporate governance at the University of Delaware, "[Y]ou’re willing to take someone’s money but not willing to invite their participation." And "[I]t makes meaningless the notion of investor democracy." Not sure I'd agree with that (and I really mean I'm not sure, i.e., not sure whether or not I agree).

The part that caught my intention was another quote in the article, from "one of his early advisers and a Facebook investor, who asked not to be identified in the run-up to the offering." Let me start with the first part of the quote:

"There is no problem he doesn’t think he can solve…"

Hmmm. Now, if my PhD student thought like this, I think a cup of coffee and a talk is in order.

Then there is the second part of the quote:

"…but he constantly tries to find the smartest people he can to give him advice. Nearly universally, he asks them, ‘Who are the smartest people for me to talk to about this?"

Ok, now we're talking. I once asked my dad what was the number 1 mistake CEOs make (he used to be one). His answer: they decision not to hire someone who is better than them. Do I think Mr. Zuckerberg avoided the trap? I think he might. After all, he hired Sheryl Sandberg (google her, if you do not know her (pun intended)). And, yes, she is very, very good. But that is just my opinion…

iBooks in LaTeX, anyone?

In case you had not noticed yet, Apple announced a rather smart move into the textbook market, among other things by releasing an app that allows you to create your own (iPad compattible) iBook.

Interesting move. But, what about all the stuff you have written in LaTeX? Ok, first the bad news: the app is not compatible with LaTeX (interestingly enough, this sparked a widespread debate on the web, immediately after the announcement). Come on, you Cupertino people, get with the program (or rather, the markup language)!

However, all is not lost: searching for some alternatives, I came across one that seems very interesting indeed. Pandoc is a program that allows you to convert documents, from one type to another. There is a catch, but it is not a big one: the document has to be of the 'markup' type. However, since pretty much any decent text editor uses markup these days, that is not much of an issue.

The very cool LaTeX stuff ...

In a recent search for a LaTeX newsletter style, I came across Gerben Wierda's TeX showcase. Basically, it is a collection of all the cool, not-so-ordinary things you can do with LaTeX, from covers to maps, from diagrams to moving pictures. Übercool is the appropriate word to use, I guess (Übergeeky being a close second, of course….).

Valuing nature

At ECCE, one of the main projects of the past years has been the development of GRESB, the Global Real Estate Sustainability Benchmark. If there is one thing that an applied economist such as myself knows, it is that it is really hard to put a number on a lot of things. And, yes, I am aware of the irony there.

But just because it is hard, does not mean it should not be done… Why? For one, without numbers, many discussions … float, and it is much harder to decide on actions. Without numbers, progress is hard to measure. And, most importantly perhaps, without numbers there often is no (real) discussion. The last point is of particular importance, because it does not apply that the numbers have to be 100% correct, all the time….

In a recent post, Adventure journal gives the floor to Yale Environment 360, who report on a project called TEEB: The Economics of Ecosystems and Biodiversity. Set up by Indian banker Pavan Sukhdev, the project follows - to some extent - in the footsteps of the (in)famous Stern report, in that it tries to a put a number on things - things being, in this case, nature.

It is worth checking out, if only to find the answer to the question Sukhdev asks: “When did the bees last send you an invoice for pollination?” You can find the report here.

Krugman on the political economy of US debt

A bit late for me to mention, but in his January 1 column, Paul Krugman reflects on the misinterpretations of government indebtness. In so doing, he raises two interesting and - importantly! - related points.

First, he discusses the costs imposed by taxes, "if nothing else by causing a diversion of resources away from productive activities into tax avoidance and evasion." Of course, in Krugman's view taxes need to be levied (mainly) to pay the interest on debt; economic growth and time will take care of the rest.

Second, he considers the importance of stable, "responsible" governments. What does responsibility mean in this respect? In Krugman's view, it is the willingness "to impose modestly higher taxes when the situation warrants it."

So is it just willingness? Or is it a different worldview that explains why some are afraid to raise taxes (modestly, as Krugman says) or not? Let's turn then, to the 'wisdom' of Wikipedia. There is a clear distinction between default, insolvency and bankruptcy. The latter, in most cases, is not relevant for governments. As Wikipedia states, insolvency "is a legal term meaning that a debtor is unable to pay his or her debts." Default, on the other hand, "essentially means a debtor has not paid a debt which he or she is required to have paid." Is that what it comes down to, then? One party is afraid of insolvency, the other of default?

Debt, true debt, debt payments and what about raising taxes?

In a recent blogpost, Bruce Bartlett, who served both Ronald Reagan and Bush Sr., discusses the US government debt. Bartlett bases his analysis on an often ignored source: the Financial Report of the United States Government, published annually by the treasury.

A couple of lessons stand out, from the analysis:

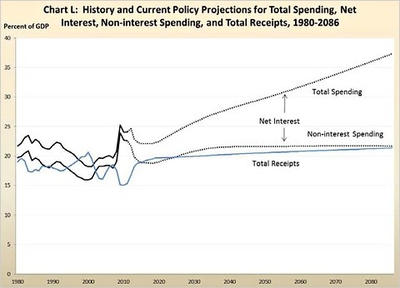

- Government debt is more than just federal debt. Much more, in fact. That may seems obvious. But wait until you read the numbers. In 2011, Federal debt (past deficits summed up, minus past surpluses summed up) was USD10.2 trillion (on September 30). However, add to that USD5.8 trillion owed to federal employees and veterans, unfunded social security liabilities of USD9.2 trilion (over the next 75 years) and Medicare's unfunded liabilities of USD24.6 trillion.

- The effect of cutting future expenses on the net debt position is marginal. To see why, consider the chart from the report, reproduced below. Most of the debt spending is on interest.

- In the words of Bartlett: "[T]he critical point is that interest on the debt is not just another government program that can be cut. It can be reduced only by running a budget surplus, selling assets to reduce principal or reducing the interest paid on the debt.

Reproduced from Financial Report of the United States Government

So what about those options? Well, interest rates are not going to drop much more (they cannot). And reducing the maturity of the debt (another way to lower interest rate payments) has already - successfully - been pursued since the Clinton years. Selling assets? Not likely given the current state of the economy.

Bartlett does not say it out loud, but the numbers suggest that raising taxes to facilitate in running a surplus and reduce the net debt position may seriously be worth considering … Especially (have another look at the above chart) since every dollar used that way will lead to a reduction in future interest spending for a long, long time…..

Lengthen your horizon, and invest ...

Yes, no typo here: I wrote lengthen your horizon, rather than broaden your horizon. It seems to me that, more and more, this is one of the important challenges that we face: how can lengthen the horizon of consumers, firms, and investors? I'm sure there's a paternalistic answer to this: regulate (read: let the rules set the horizon, for example in pension decisions). But I'm equally sure that another solution is to be preferred: what if we can create incentives for people, firms and investors to lengthen their horizon?

Why I am writing this now? Well, here's the inspiration. A piece by Adam Davidson in the NY times that describes the dangers the US faces in losing its competitive edge as a result of sharply dropping investments in R&D.

Competition and the cost of government borrowing

I've started a paper that looks at syndicated lending: the cases where a firm receives a loan from a syndicate of banks, led by one of the banks. It's a fascinating world - especially if you're interested in competition. Can collusion in this market help overcome market failure? If so, how do you know when it does?

Whatever the answer, it seems that governments may have to wrestle with a similar question … urgently. A recent Bloomberg article discussess the way governments issue bonds. Who gets to be the top underwriter?

In a recent case, in the state of Massachusetts, state treasurer Steven Grossman is quoted as saying that "[T]here's always a certain amount of competition going on out there." Had adds that "[T]hat's good. We like competition."

So do I. But how much competition is there in this market? The same article states that in the US, only "about 20 percent of debt issues by states and local governments is sold through competitive bids."

In the remaining 80 percent, so-called 'negotiated underwriting' takes place. Rolling Stone magazine, in a recent post, is highly critical of this 80 percent, citing research by University of Connecticut professors Mark Robbins and William Simonsen, who find that competitive issues lower borrowing costs.

Worthy of more attention, imho….

A bit more on Stata graphs

In a recent post, I mentioned the new edition of "A Visual Guide to Stata Graphics". In principle, I'm all for the 'notepad' approach: whenever I need to come up with a new way to display information (a table, a graph, etc.), I head for the whiteboard and try to sketch what I need.

Nevertheless, a bit of inspiration can be very helpful. Here are some suggestions…

My number one tip: Friedrich Huebler's blog called International Education Statistics. With his blog, Huebler achieves a very nice balance between form and content. I ran across the blog when looking for a nice way to make maps with Stata. Highly recommended, even if you're not interested in education statistics ;-).

Second tip: a set of Stata graph examples, reproduced by UCLA from the Stata originals. Click on each of the graphs to see the underlying code that produces the graph.

Third, the graphics section of the Stata daily blog: particularly helpful for those nasty details, like changing the color of elements of a graph, stacking graphs in unusual ways, etc.

Finally, a new development: here's a blog post on recent advances in bringing network graphs to Stata. Still requires a bit of work, but very promising.

Picture perfect: Gates Foundation Infographics

A good picture 'sells' a story. A great picture tells a story … And the best pictures make the story redundant. Finding out how to present the facts in a way that is both fair and appealing can be tough.

Looking for pictorial inspiration? Check out the Gates Foundation Infographics, here.

Should you buy what I say?

Of course not! Sometimes, however, it is not so straightforward. What do you get when you combine deep thinking, sincere entrepreneurship and smart writing? The piece just published by Outside Magazine about Patagonia's Black Friday ad. Check out the article here and make up your own mind….

Negative externalities, anyone?

A lot of my own research is about productivity, transforming inputs into outputs. Delve into this literature, and you may find some strange words (well, more than just 'some', really). Things like 'netputs' or 'badputs'. Things that would be considered 'negative externalities': the stuff that is also produced as inputs are transformed into outputs, destroying (often) someone else's value, rather than adding (to the company's) value. It's an intriguing concept, and at the core of why we impose some minimum amount of regulation on firms. But it is also hard to grasp. So, some examples (that, frankly, are not so hard to grasp) here.

A quick fix? Draghi and ECB lending

An article in the New York Times of December 22 discusses the fact that 523 banks have now borrowed a total of 489.2 billion euros ($640 billion) at the ECB's new, favorable rate.

A bit surprising, to me at least, the same article states that "[I]t turns out that may be enough to stem the European crisis for at least a few years, and go a long way to recapitalizing banks in the process."

A few years? Really?

See the article here.

What's it like to be dismal?

From my years as a bachelor student in economics, I remember two interesting questionaire results (ok, probably more than two, but that is a bit besides the point right now): first, the two best predictors of academic success in the first year of a Dutch economics student at Maastricht University (where I studied) were highschool exam grades in math and Dutch, respectively. So much for highschool economics education? I'm afraid so…

A recent paper in the Journal of Economic Behavior and Organization by Yoram Bauman and Elaina Rose reminded me of the second result: more than anything (and more than other students), my fellow economics students cared about … making money. The paper studies what, in a recent NY times oped, the authors call the Grinch stereotype.

There is good news as well (for me at least, since nowadays I teach economics): the author find that the attitude towards altruism of economics students is mostly a selection effect. In their own words, "taking economics classes did not have a significant negative effect on later giving by economics majors."

Check out the original article here. And the NY Times piece here.

New edition of "A Visual Guide to Stata Graphics"

The new edition of "A Visual Guide to Stata Graphics" is out. It's a great book with many, many (many) detailed examples of how to make great Stata graphs. Here's the link.

Al Gore on sustainable finance

In the Wall Street Journal of December 14, 2011, Al Gore has written a very interesting piece about sustainable capitalism. He cites recent work by Rob Bauer and Daniel Hann on this topic. Rob and Daniel are two colleagues of mine, both affiliated with the European Center for Corporate Engagement, ECCE.

Check out the article here

For more on the work of Bauer and Hann, see www.corporate-engagement.com

How to interpret regression coefficients

Always wonder how to interpret that coefficient after you ran your regression? Lefthand side variable is in logs, righthand side variable is a dummy. Etc, etc.

Bill Evans, at the University of Notre Dame has written a very nice document that describes the most common combinations:

http://www.nd.edu/~wevans1/econ30331/interpreting_coefficients.pdf

Stiglitz on the 1% ….

One of the eye openers for me, as an economics student, was the idea of Pareto improvement: the elegant (if not always realistic) notion of an improvement that leaves at least one person better off, without leaving others worse off. Who'd be against such a deal? The catch is, of course, that Pareto improvements often require some ex-post redistributions.

Here is a very nice Vanity Fair article by Joseph Stiglitz about (in his own words) "an inequality even the wealthy will come to regret":

http://www.vanityfair.com/society/features/2011/05/top-one-percent-201105

Also check out this